What are guarantor loans, and how do they work?

Understanding Guarantor Loans

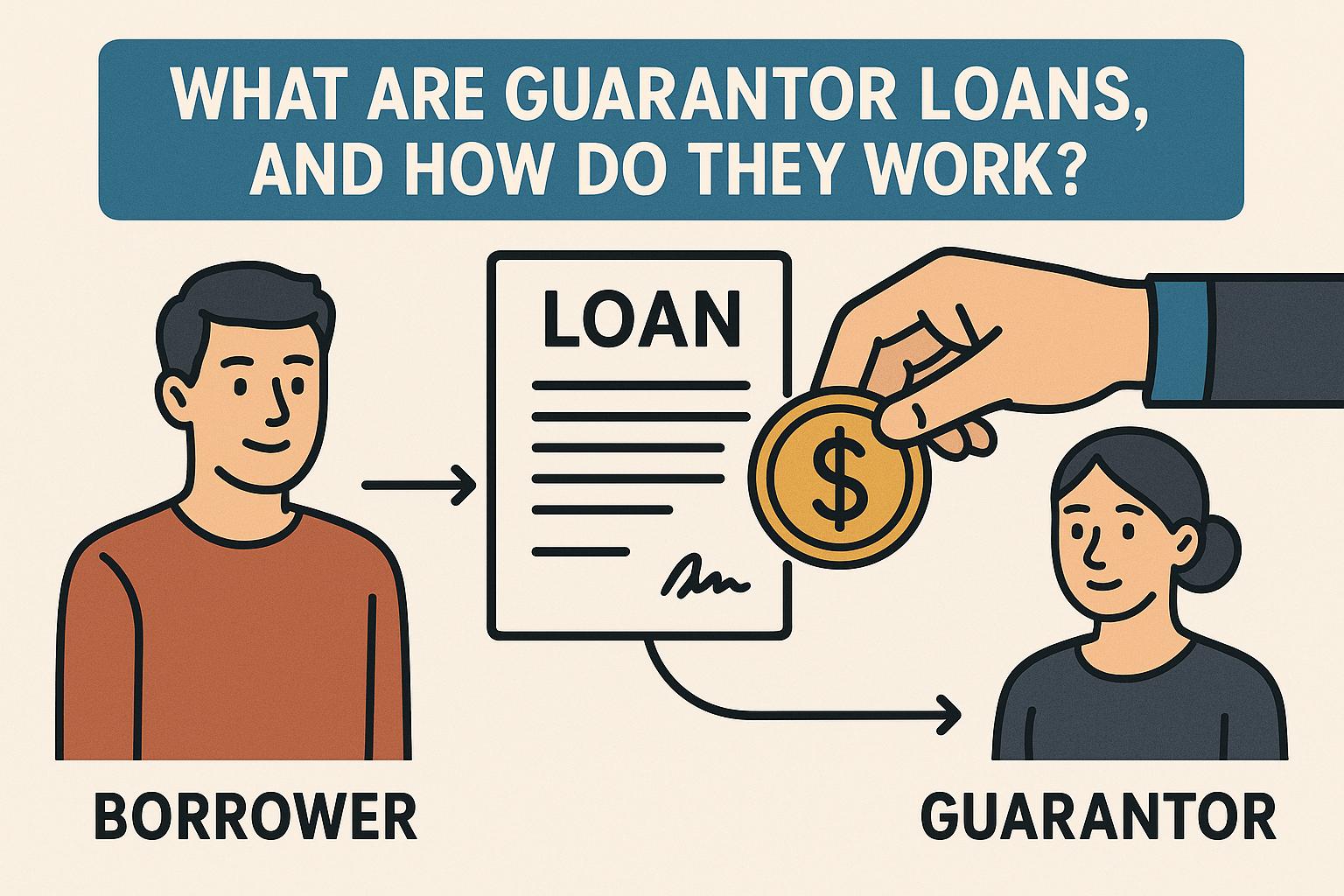

Guarantor loans present a unique option for individuals facing challenges in securing traditional loans due to poor credit histories or an insufficient credit profile. These loans involve an additional party, known as the guarantor, who commits to taking on the responsibility of the debt if the borrower fails to meet repayment obligations. This financial product plays a pivotal role in providing access to credit for those who might otherwise be excluded from standard lending markets.

How Guarantor Loans Work

The process of obtaining a guarantor loan involves multiple steps, primarily centered around the nomination of a guarantor who demonstrates both the willingness and financial ability to cover loan repayments should the borrower default. Commonly, this role is assumed by a family member or a close friend, creating a sense of trust and mutual understanding. The success of this loan type hinges on the guarantor’s solid credit score, which reassures the lender about the repayment prospects of the loan.

Steps Involved in a Guarantor Loan

Application: The initial step requires the borrower to submit a loan application, concurrently nominating a guarantor. Both parties need to satisfy the lender’s eligibility criteria, which often includes age, residency, and proof of income.

Approval: Following the application, the lender conducts a comprehensive evaluation of the financial stability and credit histories of both the borrower and the guarantor. The loan approval decision is largely influenced by the guarantor’s capacity to meet the repayment terms.

Agreements: Once approved, a formal loan agreement is executed by both the borrower and the guarantor. This legal document outlines the terms and conditions of the loan, and the borrower receives the loan amount directly.

Repayment: The borrower is expected to adhere to the agreed repayment schedule. However, in instances where the borrower defaults, the guarantor is legally obligated to cover the outstanding debt, thus safeguarding the lender’s interests.

Benefits of Guarantor Loans

Guarantor loans offer several notable advantages, particularly for borrowers seeking to enhance their credit profiles. The opportunity to demonstrate responsible credit management can lead to improved credit scores over time. Furthermore, due to the involvement of a guarantor with a potentially strong credit history, these loans often come with more competitive interest rates compared to other unsecured borrowing options available to individuals with limited access to credit.

Moreover, guarantor loans can enable borrowers to access larger amounts of credit than they might qualify for on their own, given the additional security provided by the guarantor’s promise. The structured repayment plans can further aid borrowers in financial planning and credit management, creating an opportunity for financial recovery and growth.

Potential Risks

Despite the benefits, guarantor loans carry significant risks that warrant careful consideration. The primary risk arises when the borrower defaults on the loan, thereby transferring the repayment obligation to the guarantor. This situation can impose substantial financial strain on the guarantor, who must meet the repayment terms possibly without prior financial preparation. Such scenarios can potentially damage the personal relationship between the borrower and the guarantor, especially if the arrangement was based on informal agreements.

In addition, should the guarantor also fail to make the payments, this could negatively impact their credit rating, leading to financial consequences that extend beyond their initial intent to assist. Understanding these potential risks underscores the importance of entering into such agreements with full clarity of responsibilities and a contingency plan.

Evaluating the Decision to Use a Guarantor Loan

The decision to pursue a guarantor loan should be approached with careful consideration. Prospective borrowers need to evaluate whether they have the long-term financial ability to meet the repayment schedule. Similarly, potential guarantors should consider their comfort with assuming responsibility for another person’s debt, assessing how this might impact their financial health.

A clear understanding of the loan terms and conditions is essential. This involves reviewing the repayment schedule, interest rates, and the total repayment amount over the loan’s duration. Consulting with financial advisors or conducting thorough research might also provide valuable insights into whether this form of borrowing aligns with one’s financial goals.

Guarantor’s Role and Responsibilities

The guarantor’s involvement is pivotal in the approval and administration of a guarantor loan. By agreeing to take on the repayment responsibility in case of default, the guarantor instills confidence in the lending institution regarding the recovery of the loaned amount. This assurance allows borrowers who otherwise would not meet the criteria for standard loans to gain approval.

Guarantors must be prepared for the potential financial impact of this commitment, which might involve having to pay back either a portion or the entirety of the loan amount. Ensuring their own financial stability before entering into an agreement is crucial.

Conclusion

Guarantor loans provide a viable solution for individuals who lack access to conventional borrowing opportunities but require financial assistance. Critical to the success of such loans is the financial standing and reliability of the guarantor, offering lenders increased security and confidence. However, both borrowers and guarantors should meticulously analyze the terms and take into account the associated responsibilities before committing to this arrangement.

A comprehensive evaluation of the involved risks and benefits, alongside open and honest communication between all parties, will help in making an informed decision that aligns with both current needs and future financial well-being.